A reporter asked me last fall, in a way that was either innocent or deliberate I still cannot tell, whether GM Markets was just Robinhood for tokenized assets. I had answered some version of that question maybe sixty times by then. I gave him the version I had refined down to one paragraph and we moved on. I kept thinking about it on the flight back.

The question is a reasonable one to ask, because the surface looks similar. There's a buy button. There's an order ticket. There's a list of stocks. From a screenshot, the two products look more alike than they are. I think the framing the press has settled on, that anything tokenizing equity is the consumer-app version of what brokerages already do, misses the actual product, and missing it has consequences for who builds in this space and who funds it.

So this is my attempt to lay out, without dancing around it, why the user is different, and why that difference is the actual moat.

What Robinhood solved

Robinhood is a great product. I want to be clear about that before I say anything else. The thing it solved was friction in retail US equity. It collapsed account opening from days to minutes. It collapsed commission from ten dollars a trade to zero. It made fractional shares a normal feature instead of a back-office accommodation. The aggregate effect was to bring tens of millions of new investors into the US equity market who would not otherwise have gotten there.

That is real value creation. It is also done. The thing Robinhood unlocked is now a commodity. Schwab is free. Fidelity is free. Every other brokerage has matched. The friction Robinhood removed has stayed removed across the industry, which is the highest compliment a venture-backed company can earn, and also the reason there is not a meaningful second-act business in being Robinhood for the next category.

When someone asks if we are Robinhood for tokenized stocks, what they mean, I think, is whether we are removing friction for retail US users to buy equity through a slicker interface. We are not. The friction is gone. There is nothing to remove there.

What is left to solve

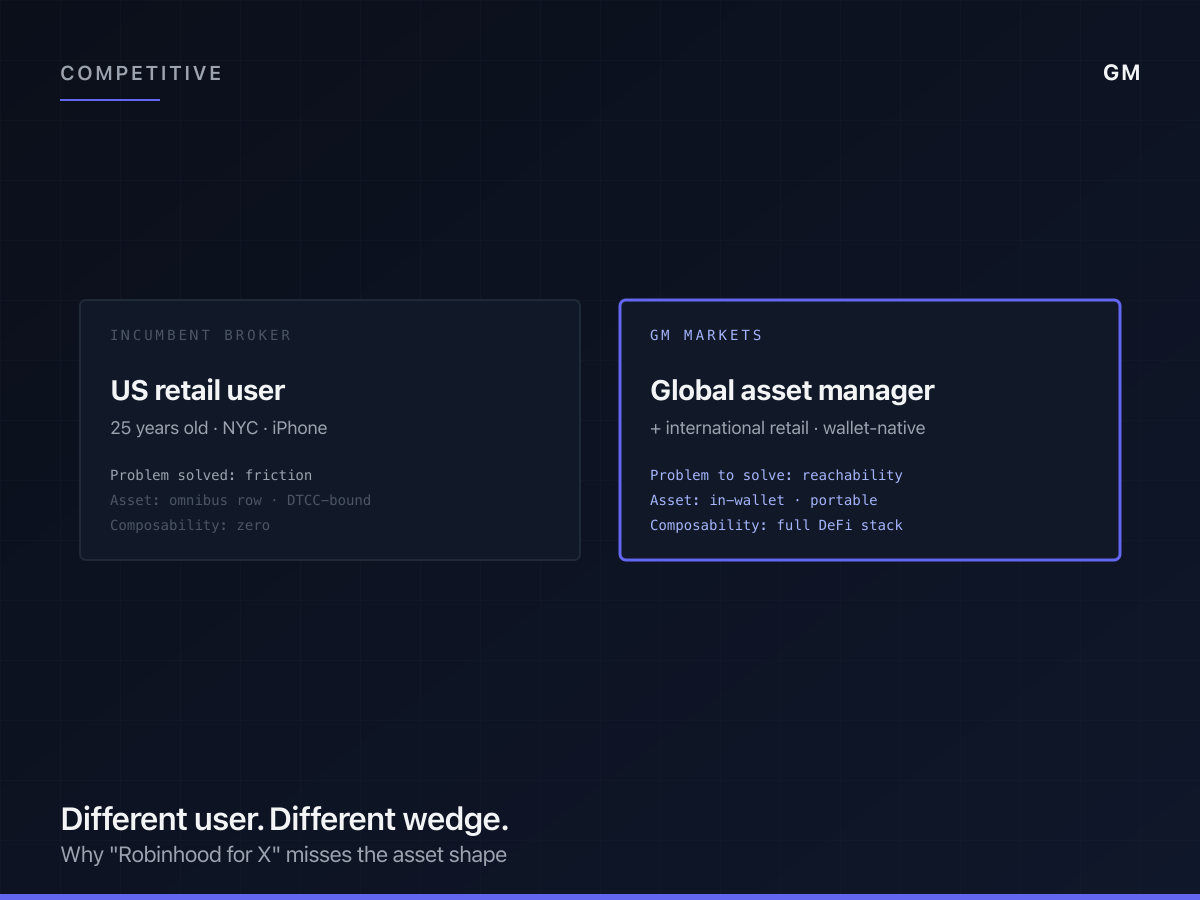

The user with a real problem in retail US equity is not the New York twenty-five-year-old. It is the user who lives outside the US, holds a non-US passport, and either cannot get a US brokerage account at all, or can get one through a Byzantine process that involves paperwork, wires, and a wait of weeks. There are many of those users. They are not the same user as the Robinhood user. They have a different problem, and the problem is reachability, not friction.

The other user with a real problem is the asset manager who runs a fund out of a non-US jurisdiction and wants to hold US equity exposure as part of a strategy. That manager is operating at a different scale, with different counterparties, on a different cadence. They have different reporting requirements. They do not want a slick app. They want something they can integrate with their existing systems, that settles into a custody surface they trust, and that does not require them to reinvent six pieces of operational infrastructure.

Both of those users have been underserved. Both of them are the user we are building for. Neither of them is the Robinhood user.

The difference is asset-shape, not feature-shape

The mistake I see most often, and the one the press question implicitly assumes, is that the two products are competing on user experience, and the user experience differences come down to interface choices. That is not the difference.

The difference is that the asset is shaped differently. A Robinhood share lives in the Robinhood omnibus account. It is a database row. It cannot leave Robinhood except by a manual transfer that goes through DTCC, takes days, and costs money. It cannot be used as collateral anywhere outside Robinhood. It cannot be moved into a yield strategy without selling and re-buying. It cannot be paid with.

A tokenized share on GM Markets lives in the user's wallet. It can move anywhere a wallet can connect to. It can be used as collateral in any DeFi protocol that accepts the token. It can be held alongside the user's stablecoin balance and treated as one portfolio. It can be redeemed, moved, lent against, hedged programmatically.

That is the wedge. It is not a feature you can ship. It is a property of the asset itself.

Why this is hard to copy

If the wedge were a UX feature, an established broker could copy it. They cannot copy a property of the asset, because copying it requires them to give up the omnibus account, and the omnibus account is the entire economic model of a broker.

The omnibus is what lets a broker net trades internally, capture rebates, run securities lending against client positions, and operate at a margin that a wallet-native model does not have. To move from an omnibus to a wallet-native model, the broker would have to give up most of those revenue lines. They will not do it voluntarily. They might do it eventually under regulatory pressure or competitive pressure. They will be late.

That is the second piece of the wedge. The thing that makes the asset valuable is the thing the incumbent cannot copy without dismantling its own business model.

Where this lands for GM Markets

I do not think GM Markets is going to displace Robinhood. Robinhood is a great product for the user it serves. It will continue to serve that user. The user-segment overlap between us and Robinhood is small enough that we are not really competing for the same flow.

What we are competing for is the asset manager outside the US, the family office in Asia or the Middle East, the fintech treasurer in Latin America, the on-chain native user who wants equity exposure inside the same surface they already operate in. That set of users does not have a default option today. Every option they have requires significant compromise. Our job is to be the default for that segment.

The reason this matters for how GM Markets gets covered, and how it gets funded, is that the framing "Robinhood for tokenized stocks" both undersells the moat and miscasts the user. It assumes the wedge is friction, when the wedge is reachability and asset-portability. It assumes the user is retail US, when the user is global asset manager and global retail. It assumes the moat is interface, when the moat is asset-shape.

I get nervous when I see the framing repeated, because it lowers the ceiling on what people imagine the company can be. The actual ceiling is much higher than "second-best Robinhood." The actual ceiling is being the venue that the next billion users of equity exposure default to, and that next billion is not in the United States.

I might be drawing some of these lines too sharply. There is a version of the future where Robinhood eventually figures out wallet-native and the wedge compresses. I do not think that version is most likely. I think the more likely version is that wallet-native equity becomes a category, GM Markets becomes the institutional default for that category, and the existing brokers continue to serve their existing user, which is fine. Categories that look like substitutes early on often turn out to be complements. We will see.

The thing I'm sure of is that the question, "are you Robinhood for X," is the one that gets asked by someone who has not yet realized X is a different X.