The most common question I get from someone who has just landed on the vaults page for the first time is: are these all doing the same thing, or different things. The answer is different things, but the page does not yet make that obvious enough, which is the kind of failure that is mostly mine.

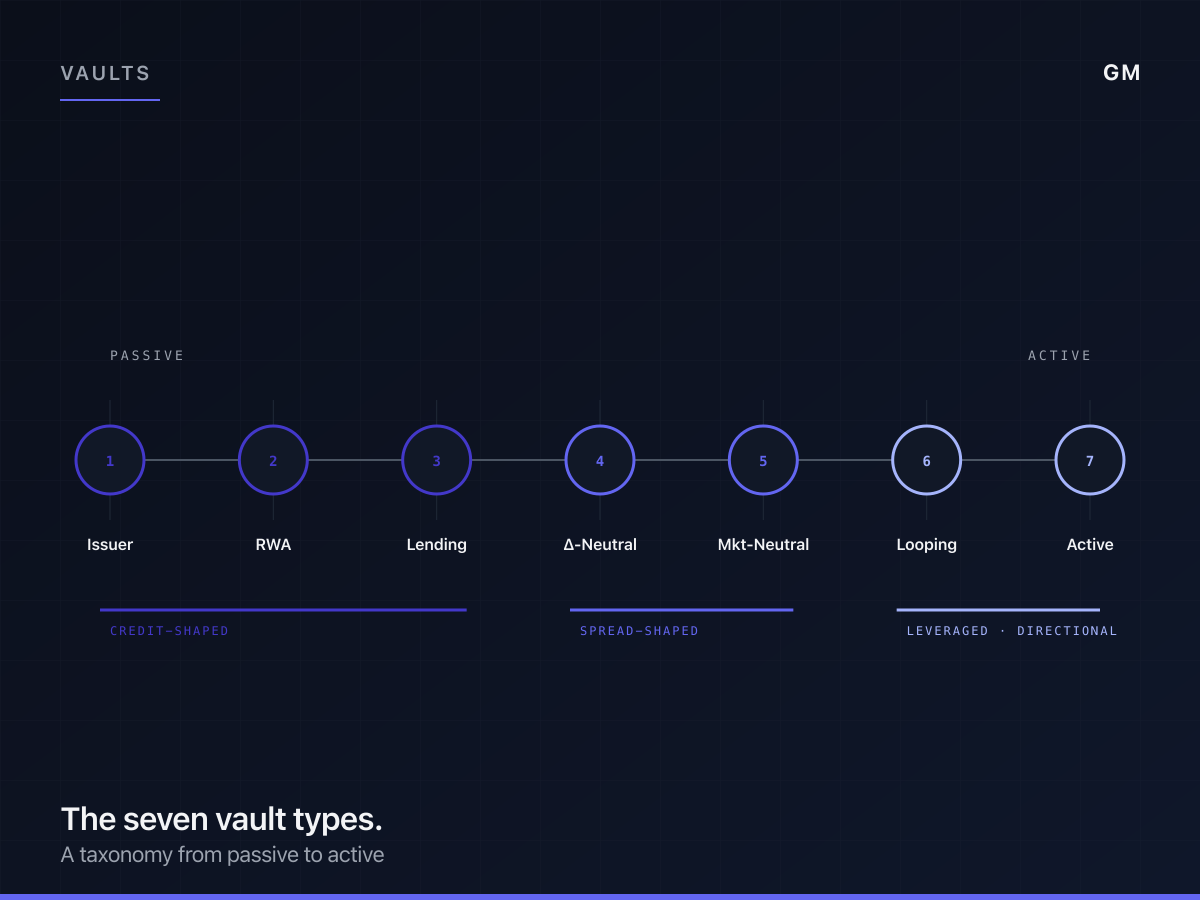

We landed on seven vault categories after a long argument about whether to collapse some of them. I think the seven is right. I'm going to walk through the categories in the order I'd recommend a portfolio strategist think about them, which is roughly from most-passive to most-active, because that's the axis that matters for risk and liquidity and is the axis the page should probably reorder around.

Category one: the issuer vault

The issuer vault is the only category in which the manager of the vault is also the originator of the underlying. The underlying might be credit-card receivables, or a basket of consumer loans, or trade finance paper. The vault sits on top of an asset that the vault operator created, in the sense of underwriting it and putting it on its own balance sheet, and the vault token is a claim on the cash flows from that asset.

The economics here are different from the other six. There is no separate manager. There is no fee split between manager and protocol. The originator captures the full spread between the funding rate and the underlying yield, less the operating cost of running the asset. From a user perspective, the issuer vault is the closest thing in the lineup to buying a senior tranche of a private credit deal directly, except the entry point is a wallet and the unit is a token.

I'd put this at the passive end of the spectrum because the user is taking credit risk on a defined pool, not strategy risk on an active manager.

Category two: the lending vault

The lending vault is a step toward active. The manager runs a lending strategy on existing tokenized collateral, sourcing deposits from the vault and deploying them into lending markets. The underlying might be on-chain credit protocols, off-chain credit funds wrapped on-chain, or a hybrid. The manager's job is to allocate, monitor, and rotate.

This is the category that most closely resembles a credit fund in its on-chain form. The risk is credit risk and rate risk. The yield is roughly stable, with occasional defaults. The manager earns a fee on the spread, and the protocol takes a cut of that fee. The user is still mostly passive, but they are taking on the manager's credit selection.

Category three: the delta-neutral vault

Delta-neutral vaults run a hedged strategy designed to harvest a structural premium without taking directional risk. The classic shape is a basis trade, long spot and short futures, which captures the funding premium between the two. There are other shapes that fit the category, including options-based premium harvesting and a few cross-exchange arbitrage strategies.

The reason this is its own category, rather than a subset of active trading, is that the risk profile is fundamentally different. A delta-neutral strategy can lose money, but the loss mechanism is not directional market exposure. It is funding inversion, basis blow-out, exchange counterparty risk, or liquidity fragmentation. The drawdown framing is different.

I think this is one of the categories users underestimate the risk on most. It has the word "neutral" in it. The neutrality is real but conditional. Worth saying loudly.

Category four: the market-neutral vault

Market-neutral is adjacent to delta-neutral but not the same. The strategy here is typically long-short equity or long-short tokenized assets, where the manager picks pairs and runs them with offsetting exposure. The objective is to capture alpha from the spread between the long and short legs, not from the direction of the broader market.

This is closer to a hedge fund's bread-and-butter strategy than delta-neutral is, and the operational requirements are higher. The manager has to make active picks. The vault has to support short legs efficiently. The risk profile depends on the manager's skill, not on a structural premium.

I keep wanting to merge this into delta-neutral and the team keeps overruling me. The team is right. The risk shapes are different enough that collapsing them would mislead users.

Category five: the active-trading vault

Active-trading vaults are the most volatile category in the lineup. The manager runs a discretionary or systematic trading strategy with directional exposure. The vault token is exposed to the manager's full P&L, with all the upside and downside that implies.

This is the category that needs the most explicit risk framing in the user-facing copy. A drawdown of fifteen or twenty percent is normal for some of these strategies. That is not a bug. The vault is doing what it said it would do. The user has to want that exposure.

The fee structure here is also different. Active-trading vaults typically run a higher management fee plus a meaningful performance fee, mirroring how a discretionary fund would charge. The protocol takes thirty percent of the fee, the manager takes seventy. The numbers are larger because the strategy is harder to run.

Category six: the looping vault

Looping vaults take a yield-bearing asset, lever it through a lending market, and repeat the cycle to amplify the underlying yield. The classic shape is taking a tokenized cash-equivalent or short-duration credit asset, lending it, borrowing against it, repeating, and capturing the spread net of the borrow rate.

The category is operationally specialized. The manager has to monitor the loan-to-value across the loop, handle deleverage triggers, and exit if the spread compresses. The yield can be meaningful in the right rate environment. It can also collapse to zero, or worse, in the wrong one.

I have been surprised by how much demand there is for this category. The simplification of "I want a leveraged version of a known yield" is appealing to a lot of users who would not run the loop themselves. The vault wrapper exists because manually running a loop is a pain, and a loop that breaks unattended is worse than not having one.

Category seven: the RWA vault

The RWA vault wraps a tokenized real-world asset that is permissioned at issuance into a permissionless wrapper. The classic shape is a senior tranche of a credit ETF, or a tokenized treasury fund, or a tokenized private credit position, that on its own can only be held by qualifying investors. The wrapper adds the layer of access control, position management, and redemption that makes the underlying composable for users who can't access it directly.

The manager here is doing something close to a fund-of-funds role, but on-chain. They source the underlying, hold it through the appropriate compliance wrapper, and distribute the economics to the vault token. The fee structure is small, because the manager isn't running a strategy. The protocol takes a smaller cut for the same reason.

This is the category that grows fastest if tokenized RWAs continue to scale. It is also the category most exposed to changes in how the underlying issuers handle on-chain wrappers, which is a regulatory question that is genuinely unresolved.

Putting them on a single axis

If I had to lay these on a single risk axis, ordered from most-passive to most-active, it would be:

Issuer. RWA. Lending. Delta-neutral. Market-neutral. Looping. Active-trading.

The first three are credit-shaped. The next two are spread-shaped. The last two are leverage- or directionally-shaped. A portfolio that wanted balanced exposure across vault types would not pick one from each. It would pick the credit shapes for the base layer, add a spread shape for diversification, and consider a leveraged or active shape only if the user's risk budget allows.

I am sure I'm drawing some of these category lines too cleanly. The boundaries between delta-neutral and market-neutral are real but fuzzy. The boundaries between lending and looping shade into each other in some structures. We will probably see vaults that don't fit neatly into one bucket and we'll have to decide whether to subdivide further or reclassify. The taxonomy is a working version, not a permanent one.

The thing I'm confident about is that the seven categories cover the strategies users are most likely to want from a tokenized capital markets venue, and each category has a distinct enough risk shape that collapsing them would do the user a disservice.